As the federal government considers a substantial rebuild program worth $70-$100 billion over the next three years, it’s worth revisiting what impact, if any, this will have on the country’s books.

To an individual, $100 billion in spending is an unthinkable amount. However, Canada has one of the biggest economies on the planet—context for any of these numbers is critical to properly evaluate their importance.

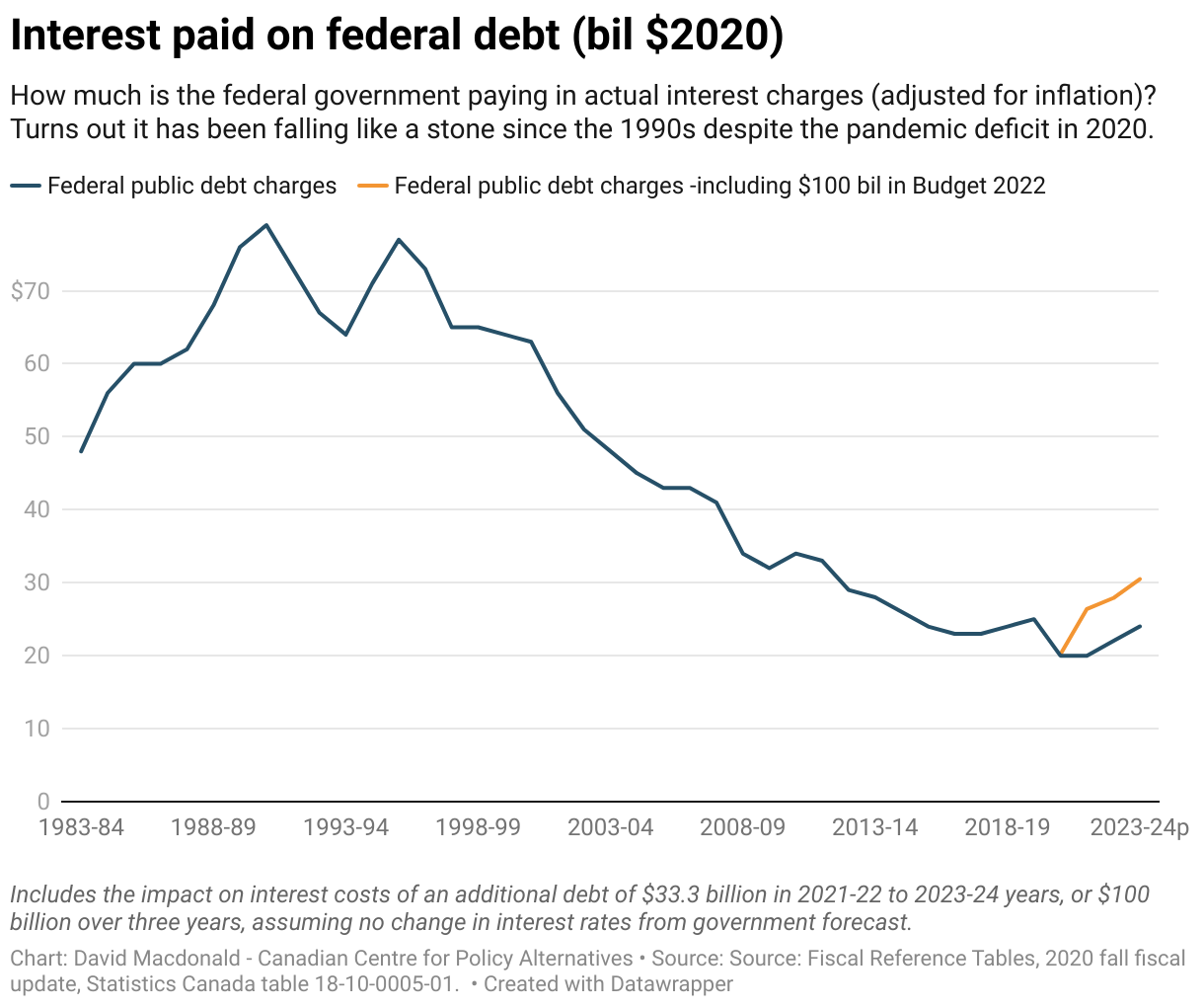

This graph looks at the actual interest paid by the federal government (in inflation-adjusted dollars) over the past 40 years (since accrual accounting).

You’ll notice that this year—the year in which a once-in-a-century pandemic necessitated massive federal spending—is also the year the federal government will spend the least on interest payments in half a century.

That interest payments include payments on the deficit from: the Canada Emergency Response Benefit (CERB), the cost of COVID-19 vaccines and massive business supports.

Let that sink in for a moment. Despite concern about deficit and debt, we’re spending a quarter of what we did on interest payments in the late-1980s. If you take into account the size of the economy, this drop in interest payments is even starker. The federal government is investing in measures to counteract a dangerous pandemic at dirt-cheap interest rates.

What we tend to forget is that when a government carries a deficit for something like protecting people from a global pandemic, they’re saving someone else from carrying that deficit—households, for instance.

In advance of the April 19 federal budget we already know that the federal government is planning to spend an additional $70-$100 billion, in addition to what’s already been announced. We can also expect that aggregate federal spending will actually decline over the next three years, as the massive pandemic supports for businesses and the jobless wind down.

If you include the high end of $100 billion over three years, you get the second line in the above graph. Yes, interest payments rise, but the change in interest owed is incredibly minor in a historical context.

In short, Canada moderated the impacts of the worst economic crisis since the Great Depression while paying less interest than at any point in past 40 years. And with an additional $100 billion, we could make major improvements in key areas, like long-term care, child care and infrastructure while still staying near the lowest interest paid in decades. It’s hard to see why we shouldn’t do that.

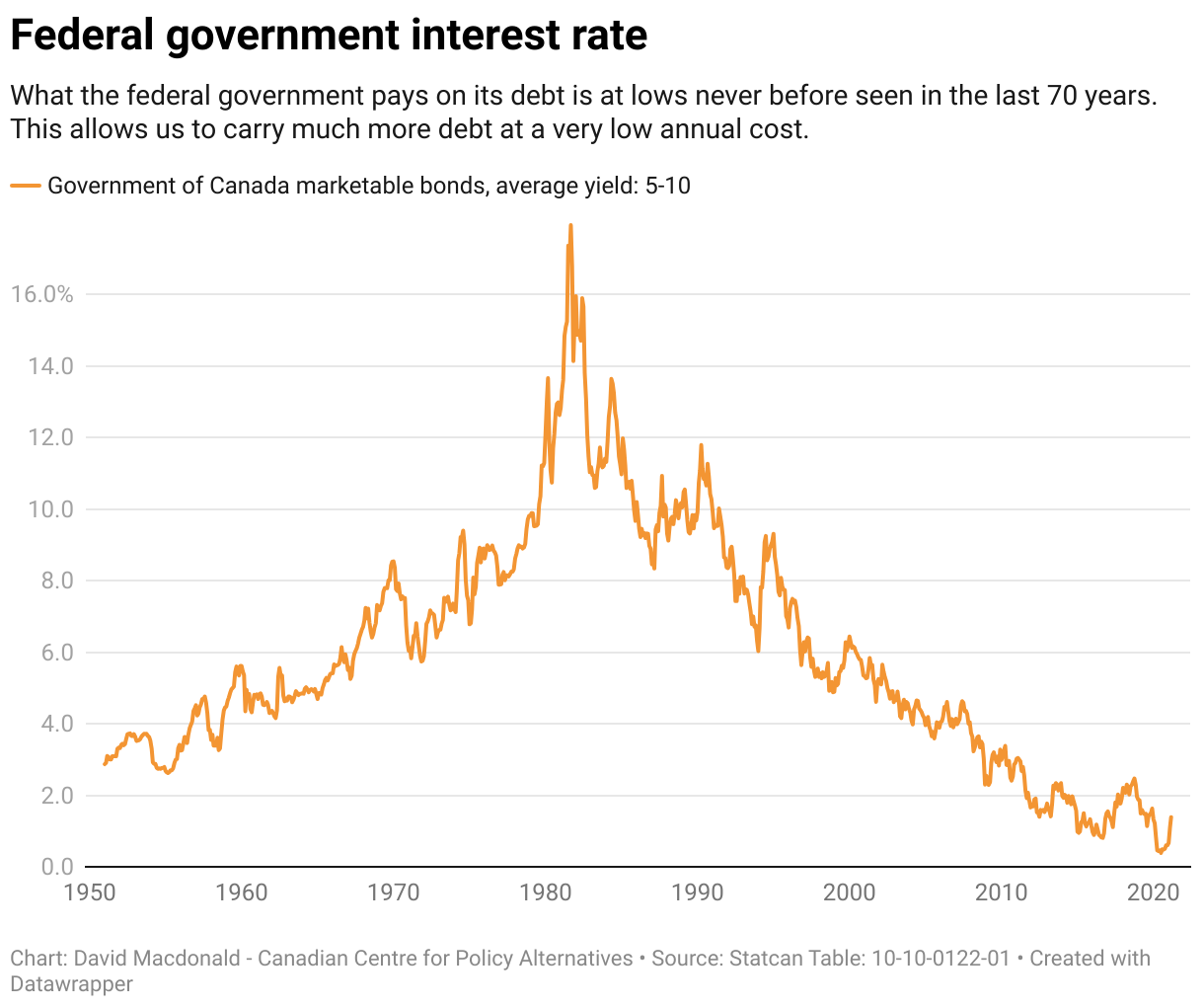

The reason why we can have a record deficit while paying less in interest than at any point in the past 40 years is because the interest rate the federal government pays hasn’t been this low since the Second World War (and possibly earlier). Since the 2008-09 recession, the federal government has also been refinancing older debt at these much lower rates.

Much ado has been made over rising interest rates in March 2021. However, any long-term examination of federal government bond yields shows how insignificant this is in context. Sub 2% interest rates on 5- and 10-year bonds have been unheard of for most of Canada’s post-war history.

It was only after the 2008-09 Great Recession that those rock bottom rates became the norm—and they remained low for over a decade, even as the economy rebounded, before dropping even further during the pandemic.

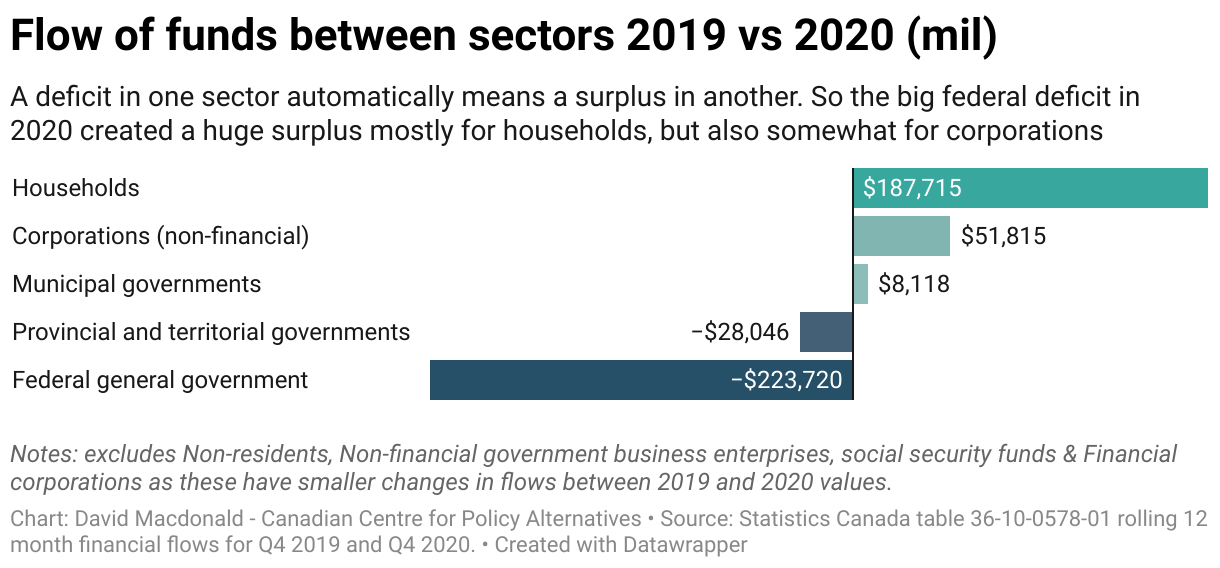

While the word “deficit” has a negative connotation, the word “surplus” has a positive one. However, both are just two sides of the same accounting transaction: one side is in deficit while the other is in surplus by the same amount. In the case of a government, if it doesn’t collect enough in taxes to cover its expenditures, it runs a deficit.

What we tend to forget is that when a government carries a deficit for something like protecting people from a global pandemic, they’re saving someone else from carrying that deficit—households, for instance. Those households are receiving more in services and transfers than they’re paying in taxes.

In that case, the household sector is in surplus by exactly the same amount the government is in deficit. They are opposite sides of the same coin.

When we include the other sectors of the economy—corporations, non-residents, provincial and municipal governments—the picture is more complicated, but it’s possible to track where all the deficits and surpluses end up. Even though there are more sectors in our economy than just the federal government and households, all deficits and surpluses still exactly offset each other. One sector’s deficit is another sector’s surplus.

The first round of federal supports was devoted to keeping money in people’s pockets as they lost working hours and jobs. This was through the CERB and its replacements, the Canada Recovery Benefit (CRB) and Employment Insurance enhancements. Plenty of support also went to business; the largest program was the Canada Emergency Wage Subsidy (CEWS), which was meant to keep employees on the payroll.

The record federal deficit-funding for these programs supported a corresponding record surplus, primarily with households—although a quarter of it ended up in corporate hands and a portion also went to cities.

Provincial deficits aided in creating these surpluses, although to a much smaller degree. The other sectors in the economy, particularly non-residents, had little change between 2019 and 2020.

Although the goal of the new federal programs was to offset the economic impact of COVID-19, there will be knock-on effects of federal deficits. The creation of these surpluses among households, in particular, will help drive the recovery once widespread vaccination is accomplished—hopefully by this summer.

There is always the risk of interest rates rising, a common bogeyman invoked by those concerned about government deficits. But rising rates would apply not just to the federal government, but to the rest of the Canadian economy. This may seem obvious, but that prospect rarely enters into the narrow discussions around federal finances.

Interest rates are most likely to go up because the Bank of Canada pushes up short-term rates that then ripple out to longer-term rates. The Bank of Canada would do that to quell inflation and drive down economic growth. While higher rates would certainly have an impact on federal finances, it would have a much more severe and immediate impact on households and businesses.

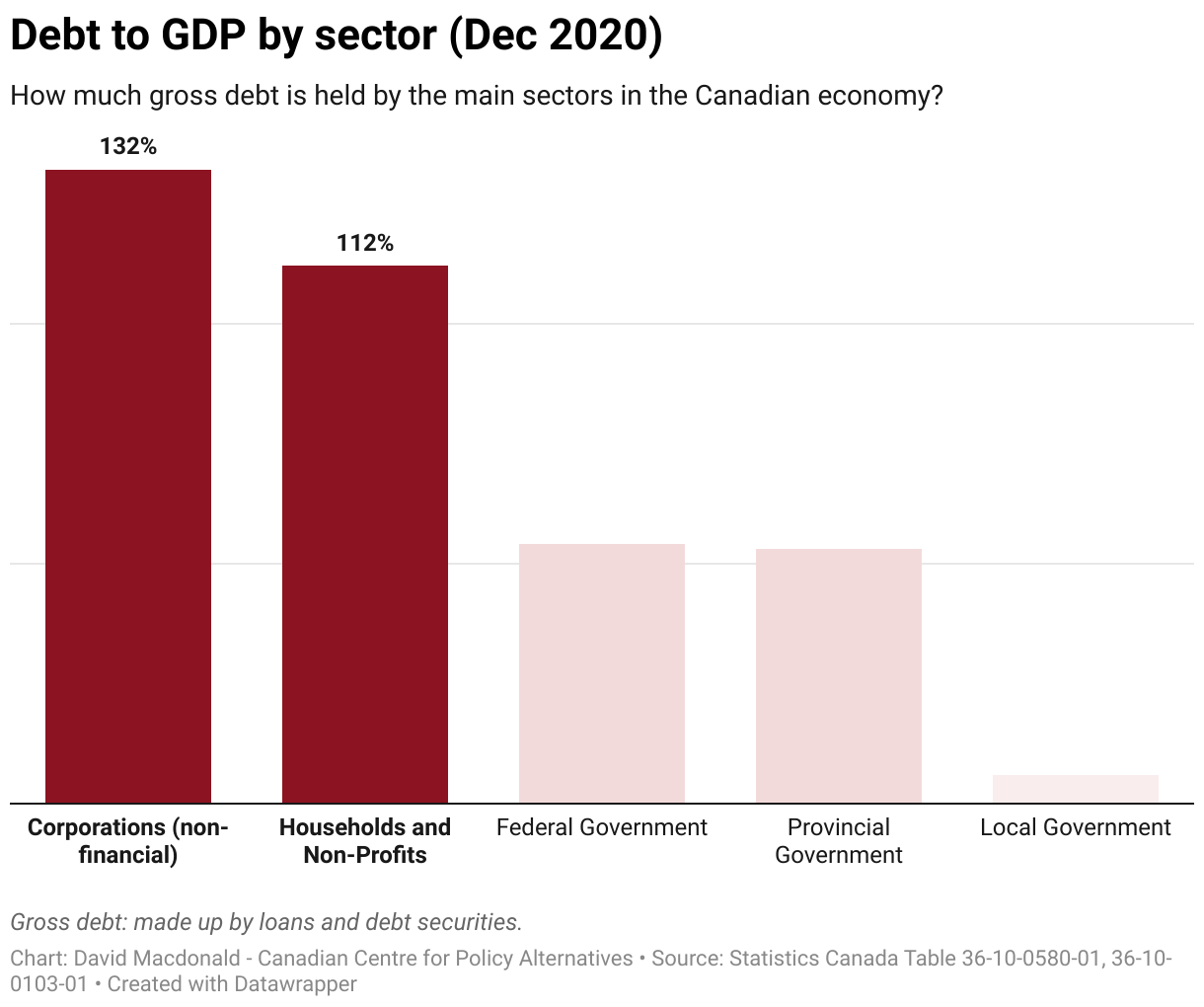

Gross federal debt in December 2020 amounts to 54% of GDP, similar to provincial debt. However, corporate debt topped both at 132% of GDP and household debt now sits at 112% of GDP. These sectors are much more exposed to interest rate changes. Not only do they have much more debt, but they pay much higher interest rates.

These heavy debt loads mean that even small changes in Bank of Canada rates have crushing impacts on economic growth. With private debt this high, interest rates simply can’t go up by much—they’d bankrupt the private sector if they did. Low federal interest rates are protected by over-indebtedness in the private sector.

It’s worth pointing out that the Bank of Canada is owned by, and takes its policy direction from, the federal government. Its marching orders from the federal government are under review right now and could be much broader than just “keep inflation low”, which is historically what they’ve been. Those orders could be modified to balance low inflation against the need for full employment, like the mandate for the Federal Reserve in the United States.

So, with record-low federal interest payments protected from increases due to dangerously high private-sector indebtedness now is the time to use federal power to rebuild better.

The pandemic has illustrated huge gaps in our social safety system, in long-term care, child care and jobless benefits.

We also need to deal with the existential threat from climate change.

Investments in all of these challenges will pay off over the years, and decades, to come. The pandemic has also illustrated the awesome fiscal power that can be wielded by the federal government when it chooses to. Now is the time to use that power to build back better.